Thank you for considering Draughts & Ledgers, Ltd for your bookkeeping needs. In order to provide you with a proposal, I need to see your actual books as they currently exist. I’ve directed you to this page because you’ve indicated that you currently use QuickBooks Online. Follow these simple instructions to share your financial information with me!

From your QuickBooks Online Dashboard, go to the Gear icon in the upper right.

Select Manage Users

Go to the Accountants tab

Enter qboa(the @ goes here)draughtsandledgers.com

That’s it! You’ve now shared your information with me in a secure way. You have the right as the account holder to revoke this access at any time. Any activity I do in your accounts is tracked & logged. At this stage, all I’m doing is taking a general survey of how things are and considering the work necessary to take them to where they need to be. Thank you for taking this step on getting your books in order and your financial life straightened out!

It has finally happened. Buried in that stack of unopened mail you’re finally getting to is that letter from the Department of Revenue. Dread sours your stomach and anxiety quickens your breath. Shaking, you open it to find a Notice of Pending Audit [- is this correct name?]. The jig is up. The pooch, hiding under the porch. You’re about to be buried by the arduous task of proving that you are innocent, racking up huge accountant & legal advice bills in the process. You don’t have time for this. Your business doesn’t have the resources for this. You don’t want to deal with this. Why is this happening to you?

Good news! This is not about you. Take a nice, deep breath. The Department of Revenue is charged with conducting random audits. There is likely* no particular reason you received this notice other than your business was selected at random. Take another breath. Unless you are knowingly violating excise or meals tax laws, the worst that will happen is that the records will be corrected and the proper amounts accessed. You’ll learn a little about how to improve your recordkeeping, make arrangements to pay what was due, and off you go.

*If you ARE knowingly violating excise or meals tax laws, fess up early and work with the DoR now that you have seen the errors of your ways. Trying to deny, obfuscate, or obstruct will only make things worse for you. Your industry peers are playing by the rules; what makes you so special?

What the DoR wants

The Department of Revenue is only interested in seeing where your submitted numbers came from and that they are nice and accurate. They will assume that your original records are factual and that the summary you make available to them reflects these facts. They are generally looking at two things: Excise Tax & Meals/Sales Tax.

Excise Tax

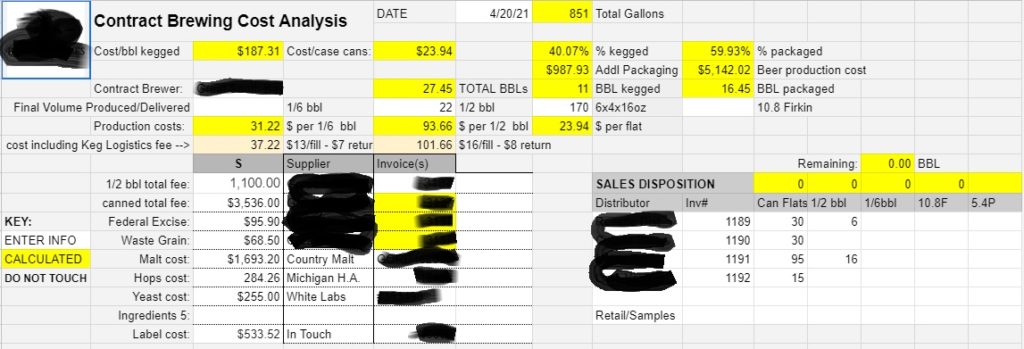

For an Excise Tax audit, your auditor wants to understand 1) where the beer came from, 2) where the beer went, and 3) that all of the beer is accounted for. Where the beer came from is generally either in-house production or contract brew acquisition. Either way, your AB-1 is going to reflect the source and, more importantly, the tax-determined volume produced. Let’s show them your calculation:

Date

Gyle/Invoice

Wort Produced (BBL)

Wasteage (%)

Packaging Date

6x4x16oz cans

1/6 BBL kegs

1/2 BBL kegs

10.6G Firkin

Total Volume Packaged (BBL)

Total Volume Packaged (Gallons)

20APR21

21PA14

18.6

21APR21

21PA15

18.5

21APR21

21PA16

18.6

3.22

10MAY21

436

30

10

52.19

1618

On your AB-1, you probably put in something like this:

Date Rc’d

Invoice#

Acquired

Number of BBL or cases

Number of liters

No tax paid (gal)

MA tax paid (gal)

10MAY21

21PA14-16

Packaged gyles 21PA14-21PA16

52.19

1618

Note that while you do not report your gyle volumes to the DoR, they like to see them on your internal summary sheet so that they can confirm that your wasteage percentage is reasonable. They are familiar with your industry and understand that a NE IPA will have higher wasteage than a British golden ale. What they’re looking for is that you aren’t “wasting” beer into clandestine packaging that’s falling off a truck at your back dock. They’ll work to confirm this by looking at your packaging and materials costs as seeing if they’re in line with industry averages. They’ll also be checking your AB-1 numbers against your quarterly federal BROP submissions.

Once the DoR understands where your finished product is coming from, they’ll want to understand where it’s going. They’ll typically do this by choosing, from your excise tax filing, a couple of lines to investigate. What they’re trying to do here is link the sales invoices to the product packaged on a particular date. Here’s an example of a log sheet I use with one of my contract brew clients.

So clearly, all product was sold on these 4 invoices. With the invoice number and your sales log, they can now cross-reference the purchaser and see that yes, the product is accounted for in and out of your brewery. If you have on-site consumption or retail sale, you’ll need to record this movement from your production (brewery) space to retail (taproom). I find it useful to recorded on $0 internal sales invoices, which will not only account for volume moved but also record the conversion of production inventory to retail COGS. I also recommend using a sales invoice to record beer used for Promotional/Advertising purposes as this beer is tax-exempt [NEEDS CONFIRMATION]

This is easier with one-off batches or discrete purchases like my contract brewing client. This is much more difficult with continuous brands, large batches, and small accounts. Hopefully you’ve been practicing FIFO and can produce a reasonable estimate. It’s much better if you already have a mechanism to track batches because if you need to do a recall due to a contamination or some other reason, you want to be able to reach the retail vendors ASAP. If you’re using a production package such as ekos_, this is all done automatically for you as their software naturally tracks by the production lot. Canadian auditors find ekos_ to be sufficiently transparent in their standard, accounting-like internal structure that their excise audits consist of allowing the auditor direct access to the software. I find this to be a compelling reason to use such products.

Sales & Meals Tax Audits

While not the focus of an Excise audit, the subject of Sales & Meals taxes may come up. Unless there’s a compelling reason to turn it over to that auditing team, they just want to do a basic check that you are:

NOT charging Sales tax on packaged beer sold at retail. This is a tax-exempt sale. And, if you have mistaken this in the past, that you correct it for future transactions and that the amounts you collected are remitted to the Commonwealth.

ARE charging Meals tax (including the local option) on beer sold for on-premise consumption.

They probably won’t check but I’d just like to remind you that

Clothing (including hats) are EXEMPT from Sales tax

Glassware (including empty growlers) are SUBJECT to Sales tax

Growlers purchased & filled on-demand are subject to MEALS tax. While the off-premise consumption of beer beer is tax-exempt, the act of pouring on demand overrides this. Since the container is incidental and included in the price, it is also subject to Meals rather than Sales tax. [NEEDS CONFIRMATION]

Growlers filled and sealed for off-premise consumption are EXEMPT from Sales tax. It must be offered without modification before sale.

If you are selling packaged goods via self-distributing wholesale or retail via the taproom, you MUST be accounting for the $.05 deposit on each container. This goes both ways; if your customer returns the empty container to you for recycling, you must return (and account for) the $.05 deposit. If your customer is a Retailer, you are obligated to issue the additional handling fee of 2.25 cents per container. [What if the customer is a restaurant? Do they get the handling fee if they never collected/returned the nickel deposit?]

Released in the first couple of days of March 2021, the updated Interim Final Rules from the December update to the CARES Act addresses a glaring flaw in the implementation of the CARES Act. This is that Sole-Proprietors were instructed to use Net Profit (Line 31 of the Schedule C) to do their calculation (Line31/12×2.5). As many small business owners know, that final ‘score’ for the year doesn’t always capture the economic benefit their business brings them. For someone with $12K here, this may not reflect the actual money-transferred-to-personal-accounts that made up your personal income. This is especially true if you’re on cash basis or in an asset-heavy business with a lot of depreciation expenses.

Let’s take that $12K net income. Under the old rules, this would be 12/12 x 2.5 = $2,500 of PPP. In my experience, many banks, especially national ones, just didn’t want to deal with the hassle of these micro-loans (their 5% Lender’s fee=$125 for processing your application and doing the loan paperwork). And, given the original requirements for onerous documentation (hope you have a good bookkeeper!), most sole proprietors took an understandable pass. Which is a shame because it was these small businesses that could have used the help the most!

Under the new rules, your calculation is instructed to consider your Gross Income instead (Line 7 of the Schedule C). Did your business generate more than $100K? You could qualify for the maximum $20,833 ($100K/12 x 2.5). This is certainly more worthwhile to pursue than the $2,500 in the example above.

Are you a contractor paid via 1099-MISC/NEC that doesn’t bother with the Schedule C? The 1099-MISC is sufficient documentation of your income for these purposes. You can probably apply based on it, whereas before it was a more difficult situation to navigate.

One thing to keep in mind is that PPP Loans CANNOT overlap any Unemployment you may have collected as a self-employed entrepreneur. For example, if you collected unemployment March-May and were able to resume business activities after that time, you should be able to specify that the PPP was retroactively for Aug-Oct. Or, for current use. Not quite sure on how the timing works out. But the takeaway here is separating the time periods.

Even if you HAVE been continuously collecting unemployment, worst case scenario is that you return the unemployment for the covered period. For example, if your unemployment was for $480/week, the 10 weeks of the 2.5 month period the PPP was active is worth $4,800. If you collected $20,833, you’re still retaining $16,033 after returning those payments to the issuing authority. You are supposed to report the PPP as income (max $2,083.30) for the weeks covered by the period. Again, this is still a developing situation but that is my understanding at this time.

I encourage you to approach your bank. Ask about the PPP application process. Cite the updated IFR. Get a piece of the aid made available to help people like you get through these challenging economic times.

A final word, *DO* expect to pay for assistance if you need it. In the original CARES Act, your assistance (Agent) was supposed to collect a small part of the bank’s Lender’s Fee and were expressly forbidden from charging you directly. The banks benefited from a previous IFR that allowed them to keep the full Lender’s Fee. A consequence of this is that Agents can now charge you directly for their services. Beware exorbitant fees and the scammers who will inevitably accompany this program. Work with someone you trust.

You also want to act fast. The PPP program ends on March 31, 2021.

Draughts & Ledgers, Ltd is proud to announce that we are now a Partner in the FreshBooks Accounting Professionals Program! It took a bit of extra training to get familiar with this neat online accounting alternative but for creatives and service entrepreneurs with modest accounting requirements, Freshbooks may just fit the bill. Designed around the all-important invoice, all of the workflow revolves around getting you paid and what you need to do to create the value you’re being paid for.

Providing a service? Direct & simple invoicing!

Selling a product? Freshbooks integrates with a variety of popular direct-selling websites in addition with giving you the flexibility to bill your wholesale accounts directly.

👇👇 Start a **FREE TRIAL** by clicking the banner below! 👇👇

Already setup in FreshBooks? Check out this short video on how to add Draughts & Ledgers as an Admin/Accountant!

Work Better Together: Accountants and Clients

With FreshBooks, accountants get access to the tools, reports, and information needed to properly advise and work with clients. This includes:

Access to accounting reports like General Ledger, Balance Sheet, and Profit and Loss

Adding Journal Entries

Managing Chart of Accounts

Reviewing and managing Invoices, Expenses, Payments, Other Income, and Bank Reconciliation

And, when it comes to tax time it’s easy to fill out and file forms. You’ll also have access to the information needed to maximize deductions and get insights into business performance.

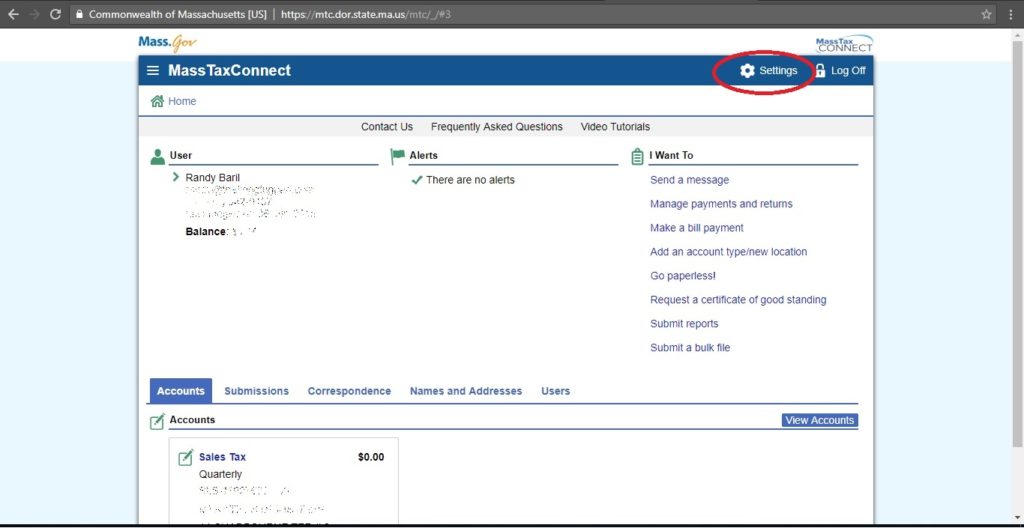

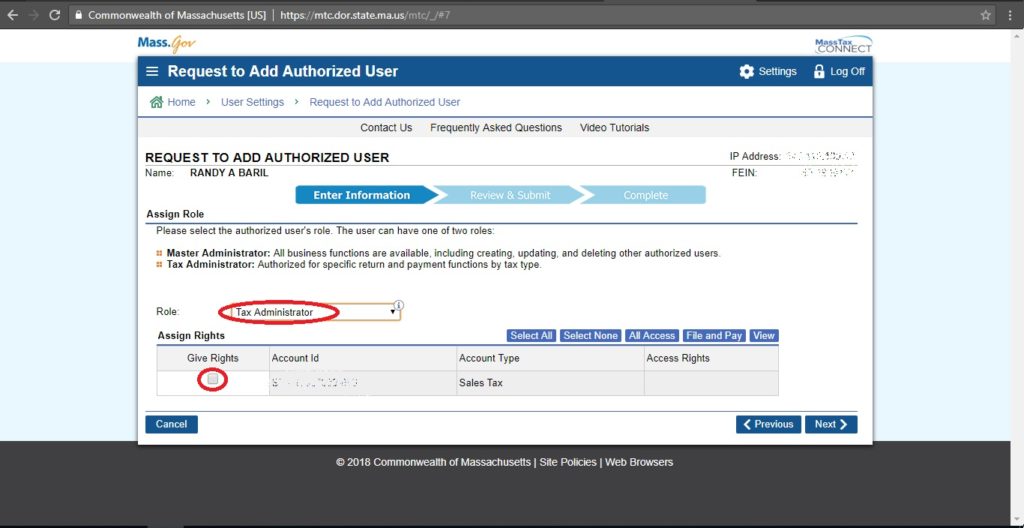

If you’re asking your bookkeeper to keep an eye on your tax status in Massachusetts, it may be helpful to give them direct access to your data in the commonwealth’s tax filing system, MassTaxConnect. Rather than share your personal Master Administrator credentials (NEVER A GOOD IDEA), set them up with their own as an Authorized User. Not only can you control which and how much access they have, their activity is logged independently by the State, which is a great deterrent of nefarious intent.

From your Home screen, click on Settings in the upper right.

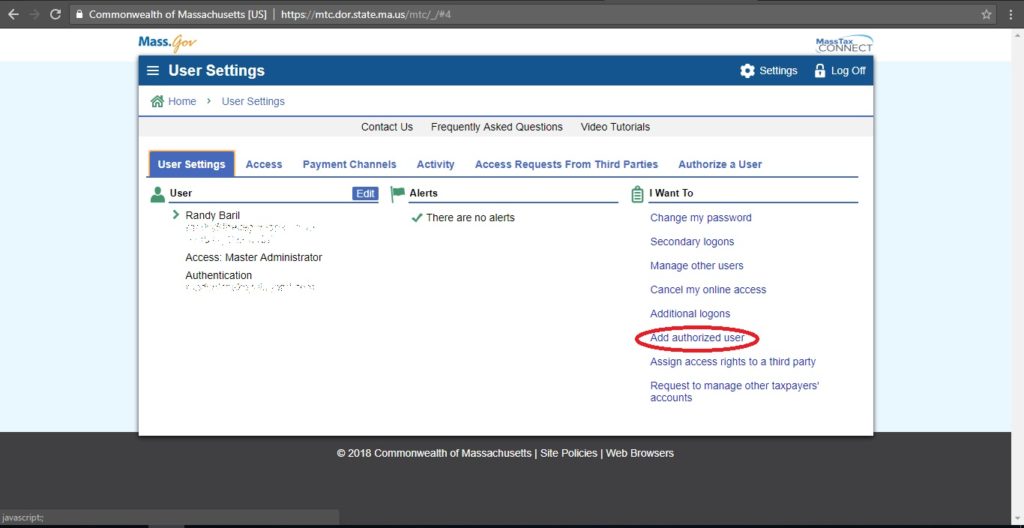

2. Select Add Authorized User on the right sidebar.

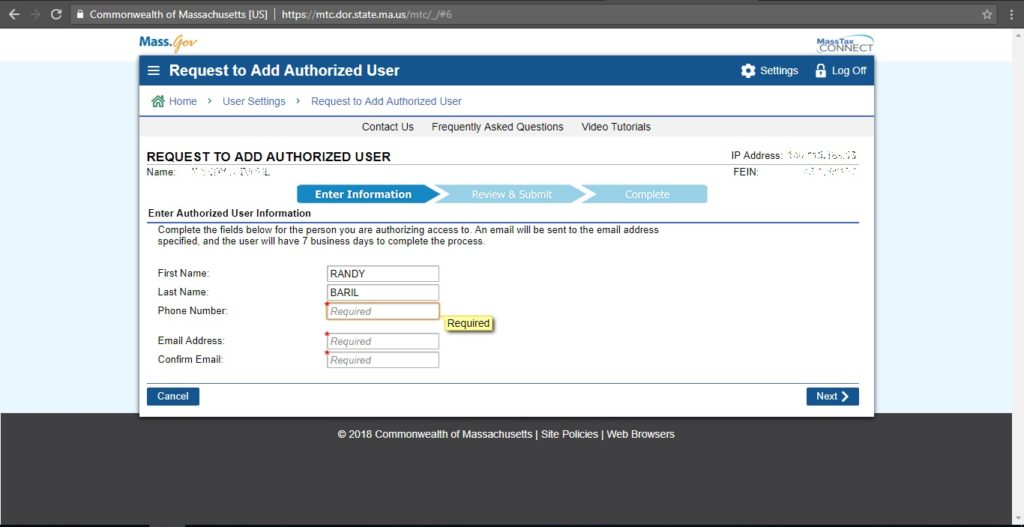

3. Enter their contact info, then select Next.

If you are entering information to make Draughts & Ledgers an Authorized User, please ask for a contact email specific to your company. To enhance security, each client gets assigned their own specific email to use in this kind of situation.

4. Select “Tax Administrator” from the dropdown and Give Rights to the appropriate Accounts once they populate. You’ll also have to grant specific Access Rights in the right-most box on each row. Once done for each Account, select Next.

View Only – Strictly for information gathering

Make Payments – For submitting payments against already-entered filings. File & Pay – For making filings, then scheduling payments. All Access – Complete rights to filing amendments, closing accounts, and doing just about everything an Administrator does.

5. Review entered data and Submit.

The data will be submitted to the system and invitation / confirmation emails will be sent.

Congratulations! You’ve allowed access to highly-sensitive information in a secure and controlled manner.

{kind=link}