** DRAFT ***

It has finally happened. Buried in that stack of unopened mail you’re finally getting to is that letter from the Department of Revenue. Dread sours your stomach and anxiety quickens your breath. Shaking, you open it to find a Notice of Pending Audit [- is this correct name?]. The jig is up. The pooch, hiding under the porch. You’re about to be buried by the arduous task of proving that you are innocent, racking up huge accountant & legal advice bills in the process. You don’t have time for this. Your business doesn’t have the resources for this. You don’t want to deal with this. Why is this happening to you?

Good news! This is not about you. Take a nice, deep breath. The Department of Revenue is charged with conducting random audits. There is likely* no particular reason you received this notice other than your business was selected at random. Take another breath. Unless you are knowingly violating excise or meals tax laws, the worst that will happen is that the records will be corrected and the proper amounts accessed. You’ll learn a little about how to improve your recordkeeping, make arrangements to pay what was due, and off you go.

*If you ARE knowingly violating excise or meals tax laws, fess up early and work with the DoR now that you have seen the errors of your ways. Trying to deny, obfuscate, or obstruct will only make things worse for you. Your industry peers are playing by the rules; what makes you so special?

What the DoR wants

The Department of Revenue is only interested in seeing where your submitted numbers came from and that they are nice and accurate. They will assume that your original records are factual and that the summary you make available to them reflects these facts. They are generally looking at two things: Excise Tax & Meals/Sales Tax.

Excise Tax

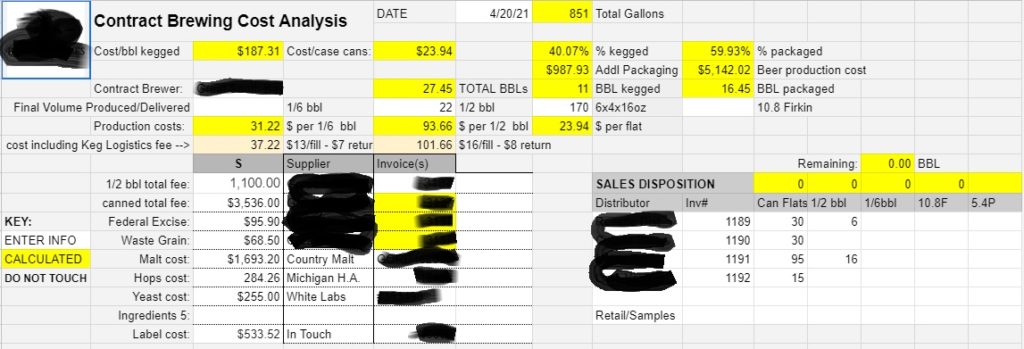

For an Excise Tax audit, your auditor wants to understand 1) where the beer came from, 2) where the beer went, and 3) that all of the beer is accounted for. Where the beer came from is generally either in-house production or contract brew acquisition. Either way, your AB-1 is going to reflect the source and, more importantly, the tax-determined volume produced. Let’s show them your calculation:

| Date | Gyle/Invoice | Wort Produced (BBL) | Wasteage (%) | Packaging Date | 6x4x16oz cans | 1/6 BBL kegs | 1/2 BBL kegs | 10.6G Firkin | Total Volume Packaged (BBL) | Total Volume Packaged (Gallons) |

| 20APR21 | 21PA14 | 18.6 | ||||||||

| 21APR21 | 21PA15 | 18.5 | ||||||||

| 21APR21 | 21PA16 | 18.6 | 3.22 | 10MAY21 | 436 | 30 | 10 | 52.19 | 1618 |

On your AB-1, you probably put in something like this:

| Date Rc’d | Invoice# | Acquired | Number of BBL or cases | Number of liters | No tax paid (gal) | MA tax paid (gal) |

| 10MAY21 | 21PA14-16 | Packaged gyles 21PA14-21PA16 | 52.19 | 1618 |

Note that while you do not report your gyle volumes to the DoR, they like to see them on your internal summary sheet so that they can confirm that your wasteage percentage is reasonable. They are familiar with your industry and understand that a NE IPA will have higher wasteage than a British golden ale. What they’re looking for is that you aren’t “wasting” beer into clandestine packaging that’s falling off a truck at your back dock. They’ll work to confirm this by looking at your packaging and materials costs as seeing if they’re in line with industry averages. They’ll also be checking your AB-1 numbers against your quarterly federal BROP submissions.

Once the DoR understands where your finished product is coming from, they’ll want to understand where it’s going. They’ll typically do this by choosing, from your excise tax filing, a couple of lines to investigate. What they’re trying to do here is link the sales invoices to the product packaged on a particular date. Here’s an example of a log sheet I use with one of my contract brew clients.

So clearly, all product was sold on these 4 invoices. With the invoice number and your sales log, they can now cross-reference the purchaser and see that yes, the product is accounted for in and out of your brewery. If you have on-site consumption or retail sale, you’ll need to record this movement from your production (brewery) space to retail (taproom). I find it useful to recorded on $0 internal sales invoices, which will not only account for volume moved but also record the conversion of production inventory to retail COGS. I also recommend using a sales invoice to record beer used for Promotional/Advertising purposes as this beer is tax-exempt [NEEDS CONFIRMATION]

This is easier with one-off batches or discrete purchases like my contract brewing client. This is much more difficult with continuous brands, large batches, and small accounts. Hopefully you’ve been practicing FIFO and can produce a reasonable estimate. It’s much better if you already have a mechanism to track batches because if you need to do a recall due to a contamination or some other reason, you want to be able to reach the retail vendors ASAP. If you’re using a production package such as ekos_, this is all done automatically for you as their software naturally tracks by the production lot. Canadian auditors find ekos_ to be sufficiently transparent in their standard, accounting-like internal structure that their excise audits consist of allowing the auditor direct access to the software. I find this to be a compelling reason to use such products.

Sales & Meals Tax Audits

While not the focus of an Excise audit, the subject of Sales & Meals taxes may come up. Unless there’s a compelling reason to turn it over to that auditing team, they just want to do a basic check that you are:

- NOT charging Sales tax on packaged beer sold at retail. This is a tax-exempt sale. And, if you have mistaken this in the past, that you correct it for future transactions and that the amounts you collected are remitted to the Commonwealth.

- ARE charging Meals tax (including the local option) on beer sold for on-premise consumption.

They probably won’t check but I’d just like to remind you that

- Clothing (including hats) are EXEMPT from Sales tax

- Glassware (including empty growlers) are SUBJECT to Sales tax

- Growlers purchased & filled on-demand are subject to MEALS tax. While the off-premise consumption of beer beer is tax-exempt, the act of pouring on demand overrides this. Since the container is incidental and included in the price, it is also subject to Meals rather than Sales tax. [NEEDS CONFIRMATION]

- Growlers filled and sealed for off-premise consumption are EXEMPT from Sales tax. It must be offered without modification before sale.

- If you are selling packaged goods via self-distributing wholesale or retail via the taproom, you MUST be accounting for the $.05 deposit on each container. This goes both ways; if your customer returns the empty container to you for recycling, you must return (and account for) the $.05 deposit. If your customer is a Retailer, you are obligated to issue the additional handling fee of 2.25 cents per container. [What if the customer is a restaurant? Do they get the handling fee if they never collected/returned the nickel deposit?]